After reviewing my first blog post there are a few topics I think need further discussion.

I talked about tracking systems that have a statistically significant edge in the market, but what exactly does that mean? How can I track my system efficiently without bias? And If I have a system that profited in the past, how can I know it will work in the future?

I also want to discuss the Kelly Criterion and the theoretical vs practical application of it to trading.

Some believe that past results cannot predict the future. My opinion is that IF these results happened in the past, there is a possibility it could occur again. If we can rule out randomness or luck with enough certainty then its worth the risk to assume it will behave similarly over a large enough sample going forward. The key here is to understand WHY something occurred in such a fashion and why it should continue behaving that way.

Ever notice at the roulette wheel there is a big screen with the results of the past spins? The casino offers you this information in hope that you will attempt to identify a pattern in the short term and make the assumption that similar results will follow. Same thing in the sports handicapping world. Team trends and other data are readily available and are even provided by sportsbooks.

They do this because they know small samples of data will likely have large amounts of variance and hope people make conclusions based off that. If they were to give the results for the past 1000 spins or games it wouldn’t be as effective since the “truth” would be revealed. This is where the law of large numbers comes in. It states that the average of the results obtained from a large number of trials should be close to the expected value, and will tend to become closer as more trials are performed. But how much is “large”? And this is subjective and depends on the type of system you are tracking. If tracking a system with a theoretical win rate of less than 10% then in my opinion you should have at least 200 data points. If the win rate is closer to 50% then at least 100 data points is required. Now the number here is personal preference, some prefer more concrete data to draw conclusions from. Others are comfortable with less data and a higher probability their results are from chance or coincidence. Personally I’m comfortable using smaller samples. I like to have a theoretical reason WHY something happened, and a thesis as to why it will continue to happen.

Say you tracked a long system that worked better in the morning vs mid-day. All the criteria are the same but the only difference is the time of day. You would theorize that the volume is higher in the morning, more people are aggressive trying to reach profit targets for the day, there is more follow through, etc. As long as you have confidence in your assessment and think it will continue to happen then its a safe assumption. Avoid “looking” for things to match your criteria or to have better backtested returns. If you cant explain logically why something occurred in that fashion, then there is a good chance you are ‘data mining’.

Historical data is everything, its how we draw conclusions and make sense of things in every aspect of life, not just in trading or sports. Our brains are constantly using “historical data” to assess situations, keep us safe from danger, etc. We as humans use the past to help guide our future, we take the best path possible based on previous experiences. I am a firm believer that history repeats itself in the stock market, just like it does in sports markets. The key is having enough data that is free of unsound bias.

Another argument against using historical data is the efficient market hypothesis. It states that asset prices fully reflect all available information, thus making it impossible to beat the market. I dont believe any market is 100% efficient, or even close to that number. If it were we would not have such volatility in stock prices or odds in sports markets. My opinion is that markets range in level of efficiency. In the sports world you have the main wagers (ATS- against the spread, ML – moneyline, and OU – over/under) that gets the majority of the attention and wagers. More money, more attention, more people involved, that generally meant the lines were more efficient and that was reflected with less volatility in the odds movements and higher wager limits as books were more confident in the lines. Then you would have the side wagers (player props, futures, team totals, etc) which would get much less attention and hardly any money. These were the plays that I targeted since they were much less efficient. You could consistently find edges in the lines because you had a legitimate chance of handicapping the lines better than the sportsbooks. Because of that they limited wagers quickly and had wide spreads on the lines (vigorish). Even with those drawbacks I had most of my success in smaller markets. These are comparable to small caps in the stock market. The lack of efficiency is displayed by the huge volatility in price movements. Big money players don’t bother with small caps and its displayed by the lower volume (money) these stocks get in the markets compared with large caps. The point here is to find the area of your niche with the lowest amount of efficiency and only take those opportunities. Dont make things hard on yourself by targeting the stocks that are likely the most efficient. Doing all these little things will add to your edge and conviction level.

Practical Application of the Kelly Criterion:

In my first post I talked about fractional Kelly stakes and how it relates to volatility. I recommend using fractional stakes as it is much easier psychologically to deal with and more practical in application.

Take the following systems for example:

System 1

Win rate: 50%

Profit Ratio: 2:1

Profit Target: 10%

Stop Loss: 10%

Edge: 50%

Kelly Stake: 25%

Expected Growth: 6.07%

System 2

Win rate: 75%

Profit Ratio: 1:1

Profit Target: 10%

Stop Loss: 20%

Edge: 50%

Kelly Stake: 50%

Expected Growth: 13.98%

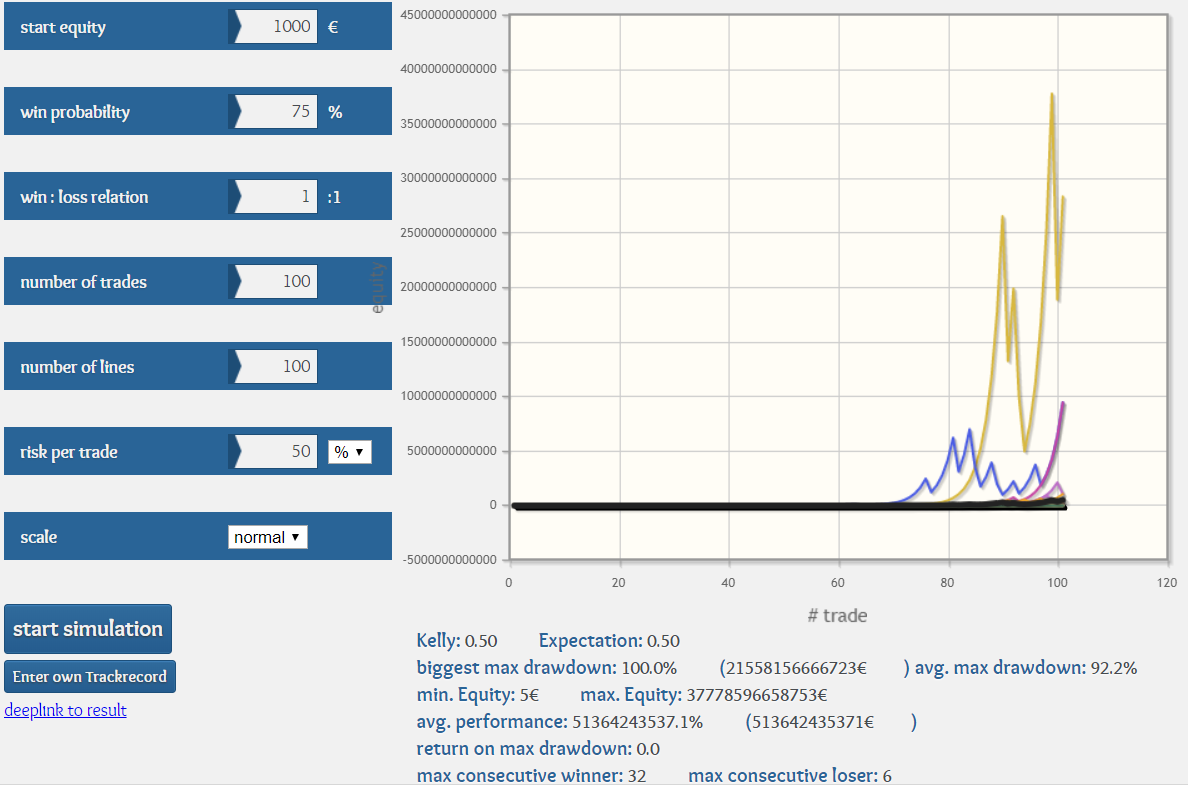

The expected growth for System 2 is more than double even when the edge is the same. We determined that to be from the higher win% and compounding factor. With a Kelly stake of 50%, that means we should risk HALF our bankroll on each trade. I just want to clarify that means we should be willing to lose that amount, so with a 20% stop our actual position size should be 2.5x our bankroll. Here is what that looks like when simulated:

Notice the max avg drawdown is 92%, that means over a sample of 100 trades you are likely to lose most of your bankroll if risking a full Kelly stake of 50% per trade. Although this is mathematically the optimal amount to risk it may not be practical for most people. The idea behind Kelly is that you are just trying to “hang around” until you go on a winning streak and that is when your bankroll will go parabolic. The swings and volatility are extreme which is why half Kelly is recommended:

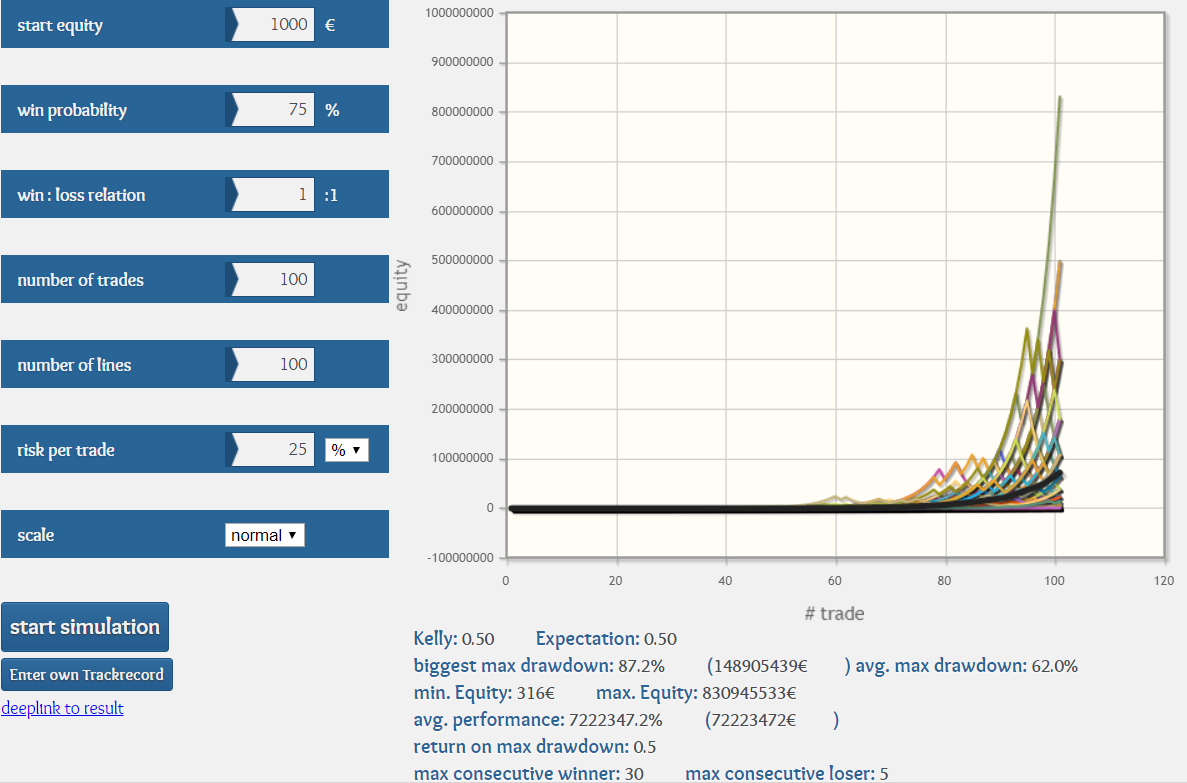

When using half Kelly we reduce our volatility quite a bit with a avg max drawdown of 62%. Still quite a bit for some people but more manageable. With half Kelly we reduce volatility by 50% while retaining 75% of optimal returns.

Another key point of fractional Kelly stakes is that you will never risk more than the optimal amount. From my previous post I showed that risking more than full Kelly will result in decreased returns and risking more than 2x Kelly will actually result in negative returns. Its common to over-estimate our edge and when you factor in slippage, commisions, partial fills on winners vs always filling completely on losers, etc. the actual stake% is always lower. By using fractional Kelly stakes you will protect yourself from risking too much.

As you can see the returns are quite impressive when using the Kelly formula and it shows you the power of compounding. Its amazing how much you can grow an account with just the slightest edge. Here is an example of a simulation with 10% risk per trade and only a 10% edge.

And the same system over 1000 trades:

The bottom line is that only a small edge in the marketplace is required to grow your account exponentially if you manage your risk efficiently and use the power of the Kelly Criterion and compounding in your favor.

Try running simulations to see what you are comfortable with.

http://www.equitycurvesimulator.com/

Best of luck,

Kris Verma